1. Introduction and Purpose

1.1.Purpose

The PRAKARSA invites NGOs acitvists and journalists to collaborate in submitting proposals to deliver investigative research in Asian countries on the taxation issues in the area of illicit financial flows, tax evasion and tax avoidance in the Asian countries specifically on extractives, plantation, and marine sectors

1.2.Issuing Office and contact person

The PRAKARSA : Komplek Rawa Bambu 1 Jl. A No. 8-E, Kel/Kec. Pasar Minggu Jakarta Selatan, Indonesia 12520

Contact : Panji TN Putra

Phone : +62 82140351543

Email : pputra@theprakarsa.org

1.3.Type of Award Anticipated

The Prakarsa anticipates awarding a Firm Fixed Price Subcontract. This award type is subject to change during the course of negotiations and the the price offer is up to IDR 200,000,000 (two hundreds million rupiah)

2. General Instructions to Offerors

2.1.General Instructions

Who can Apply? This call for investigative research proposal is design to create a collaboration between journalists and CSOs in Asia. The participant of call for research proposal have to be a group of journalists and CSOs. PRAKARSA will select three best proposals submitted based on the selections criteria.

Offerors wishing to respond to this RFP must submit proposals, in English, in accordance with the following instructions. Offerors are required to review all instructions and specifications contained in this RFP.

Issuance of this RFP in no way obligates PRAKARSA to award a subcontract or purchase order. Offerors will not be reimbursed for any costs associated with the preparation or submission of their proposal. PRAKASA shall in no case be responsible or liable for these costs.

Proposals are due no later than January 17th, 2021 5pm GMT to be submitted to perkumpulan@theprakarsa.org. Late offers will be rejected except under extraordinary circumstances at PRAKARSA’s discretion. The submission of a proposal to The PRAKARSA in response to this RFP will constitute an offer and indicates the Offeror’s agreement to the terms and conditions in this RFP and any attachments hereto. PRAKARSA reserves the right not to evaluate a non-responsive or incomplete proposal.

2.2.Proposal Cover Letter

A cover letter shall be included with the proposal with a authorized signature of the applicants (NGOs and Journalists). The cover letter shall include the following items:

- The Offeror will certify a validity period of (90) days for the prices provided.

- Acknowledge the solicitation amendments received.

2.3.Questions regarding the RFP

Each Offeror is responsible for reading and complying with the terms and conditions of this RFP. Requests for clarification or additional information must be submitted in writing via email to the Issuing Office as specified in the Synopsis above. No questions will be answered by phone. Any verbal information received from PRAKARSA’s employee or other entity shall not be considered as an official response to any question regarding this RFP.

3. Instructions for the Preparation of Technical Proposals

Technical proposals shall include the following contents:

- Technical Approach— Description of the proposed services which meets or exceeds the stated technical specifications or scope of work. The proposal must show how the Offeror plans to complete the work and describe an approach that demonstrates the achievement of timely and acceptable performance of the work.

- Management approach— Description of the Offeror’s team involved to the activity. The proposal should describe how the proposed team members have the necessary experience and capabilities to carry out the Technical Approach.

4. Instructions for the Preparation of Cost/Price Proposals

Provided in Attachment: Price Schedule, is a template for the Price Schedule for firm-fixed price awards. For cost-reimbursable or time & material awards, the offeror shall provide a fully detailed budget.

Offerors shall complete the template including as much detailed information as possible. It is important to note that Income Tax and Value Added Tax (VAT) shall be included on a separate line. The Subcontractor is responsible for all applicable taxes and fees, as prescribed under the applicable laws for income, compensation, permits, licenses, and other taxes and fees due as required.

5. Basis of Award

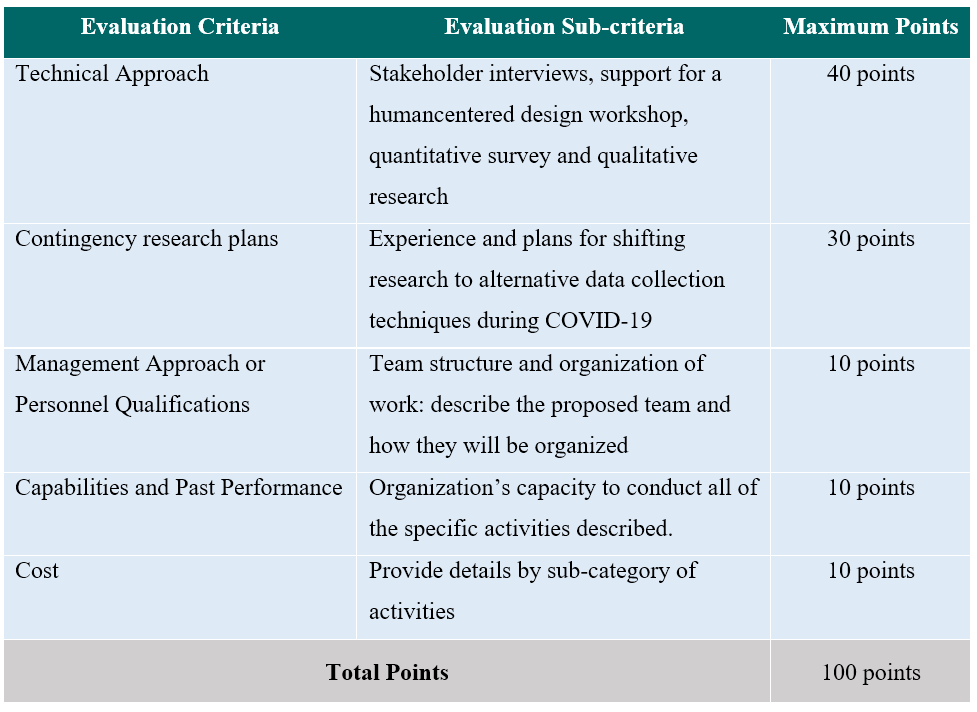

5.1.Evaluation Criteria

Each proposal will be evaluated and scored against the evaluation criteria and evaluation sub-criteria, which are stated in the table below:

5.2.Best Value Determination

PRAKARSA will review all proposals, and make an award based on the technical and cost evaluation criteria stated above and select the offeror whose proposal provides the best value to PRAKARSA. PRAKARSA may also exclude an offer from consideration if it determines that an Offeror is “not responsible”, i.e., that it does not have the management and financial capabilities required to perform the work required. PRAKARSA may award to an Offeror without discussions. Therefore, the initial offer must contain the Offeror’s best price and technical terms.

6. Antisipated post-award Deliverables

Upon award of a subcontract, the deliverables and deadlines detailed in below table will be submitted to PRAKARSA. The Offeror should detail proposed costs per deliverable in the Price Schedule. Deliverables must be submitted to and approved by PRAKARSA before payment will be processed. In general, the step for the Investigative Research on Taxation Issues submission process includes the Preparation, Investigative research, Reporting, and Publication.

- Preparation : The preparation process includes submitting the final investigative Research on Taxation Issues proposal to PRAKARSA, and other administrative processes (if accepted).

- Investigative research: Initiate research and investigation in the field, collect data, and process data

- Reporting: Write and analyze the report process.

- Publication: Each research team will publish the research report on their media, organization platforms and other publication platforms. In addition, the full report will be pulished in the PRAKARSA’s website.

7. Compliance with Terms and Conditions

General Terms and Conditions: offerors agree to comply with the general terms and conditions for an award resulting from this RFP. The selected Offeror shall comply with all Terms and Conditions listed in Attachment: Terms and Conditions.

8. Procurement Ethics

Neither payment nor preference shall be made by either the Offeror, or by any PRAKARSA staff, in an attempt to affect the results of the award. PRAKARSA treats all reports of possible fraud/abuse very seriously. Acts of fraud or corruption will not be tolerated, and PRAKARSA employees and/or subcontractors/grantees/vendors who engage in such activities will face serious consequences. Any such practice constitutes an unethical, illegal, and corrupt practice and either the Offeror or the PRAKARSA staff may report violations to the Toll-Free Ethics and Compliance Anonymous Hotline at +62(0)21 7811798. PRAKARSA ensures anonymity and an unbiased, serious review and treatment of the information provided. Such practice may result in the cancellation of the procurement and disqualification of the Offeror’s participation in this, and future, procurements. By submitting an offer, offerors certify that they have not/will not attempt to bribe or make any payments to PRAKARSA employees in return for preference, nor have any payments with Terrorists, or groups supporting Terrorists, been attempted.

9. Plagiarism and Originality

Plagiarism is presenting someone else’s work or ideas as your own, with or without their consent, by incorporating it into your work without full acknowledgement and it is an act of fraud. The Prakarsa will not tolerate any act of plagiarism and it will result in a termination of the ongoing contract. Proposal and report have to describe high-quality and original research that have not been published in any platforms.

10. Attachments

10.1.Scope of Work for Services or Technical Specifications

Perkumpulan Prakarsa believes that taxes are vital for the source of state income, an instrument to reduce inequality and enforce independence. The budget is also very important for the development and progress of the nation. Unfortunately, tax and fair budget (fiscal justice) are still far from expectations. Tax revenue is still far from optimal and the priority of budget policy that is still not appropriate is the challenge that must be faced at this time.

The study and research of fiscal justice has been outlined in the form of books, policy briefs, policy reviews, factsheets and audio visuals. The Pro-Poor Budget (2009) and the Pro-Poor Budget: A Guide for Journalists (2012) is a pioneering publication on a siding budget in Indonesia. Perkumpulan Prakarsa which includes the Global Network Alliance for Tax Justice is also involved in publishing the Tax Justice Advocacy Toolkit which has now also been translated into Indonesian.

Extractives, plantation, and marine sectors supposedly provide livelihoods for Indonesian population. However, for decades these three sectors have become a major source of profit for corporations without generating real improvement of the welfare of communities. In many resource-rich provinces, poverty rates are high and local residents receive little or no benefits from the exploitation of the country’s abundant natural wealth. Morover, they contribute less than one out of every ten dollars of revenue received by provincial and national governments (Ross, 2018).

Illicit financial flows in the three sectors have harmed economic growth due to revenue losses. Data retrieved from BPS (2017) shows that poverty rates in the provinces where the three sectors are dominant are considerably high. Prakarsa (2019) calculates that the potential revenue loss from the plantation (palm oil, coffee and rubber) amounted to USD$76 million, extractives (coal) amounted to USD$42 million, and marine (crustaceans) amounted to USD$5 million. Researches that have been conducted on tax avoidance and evasion in these sectors are like a tip of an iceberg. What have been investigated and published by the government and others are only a small part of the real situation. Therefore, further studies in the extractive and plantation as well as the marine sectors are necessary.

As an effort to encourage more studies on illiciti financial flows, tax avoidance and tax evasion in extractive, plantation and marine sectors in Indonesia, the PRAKARSA would like to invite journalists and CSOs in Asia to collaborate in “Call for Investigative Research Proposal for Journalists and CSOs.” PRAKARSA believes that the press is an objective and educational media and means of dissemination of information, constructive social control, channeling people’s aspirations, and expanding communication and community participation as supporters in national development. Meanwhile, CSOs are regarded as important sources of social innovations to address public problems. Thus, channeling these two parties in a collaborative investigative research would result a strong evidence based on the issue of taxation based on investigative researches that will publicly discussed among actors to support advocacy process.

10.1.1. Objectives of the RFP

The objective of the RFP is to produce collaborative investigative researchs on illicit financial flows, tax avoidance and tax evasion in extractive, plantation and marine sectors. It is expected that strong evidence based research and collabrative works between CSOs and journalists can create public discussion and support advocacy process to the government.

10.1.1. Purposes of the RFP:

- To obtain evidence based report of the taxation issues including illicit financial flows, tax avoidance and tax evasion in the three sectors in Asian countries through investigative research.

- To strengthen collaborative works between CSOs and journalists in Asia

- To leverage research and publication on tax illicit financials, avoidance and tax evasion in the three sectors

- To increase public awareness in order to build public pressure on illicit financial flows, tax avoidance and tax evasion in the three sectors through media.

10.1.2. Scope of topics

The call aims to provide grants for investigative research on taxation issues (tax evasion, tax avoidance, illicit financial flows) in the following focus areas:

- Extractive sector

- Plantation sector

- Marine sector

10.1.3. Location of Work

The location of the research is in Asian countries that involved 10 areas of work in Indonesia, they are:

- Sumatera Utara

- Riau

- Sumatra Selatan

- Jambi

- Sulawesi Selatan

- Kalimantan Barat

- Nusa Tenggara Barat

- Jawa Timur

- Jawa Barat

- DKI Jakarta

10.1.4. Duration of consultancy

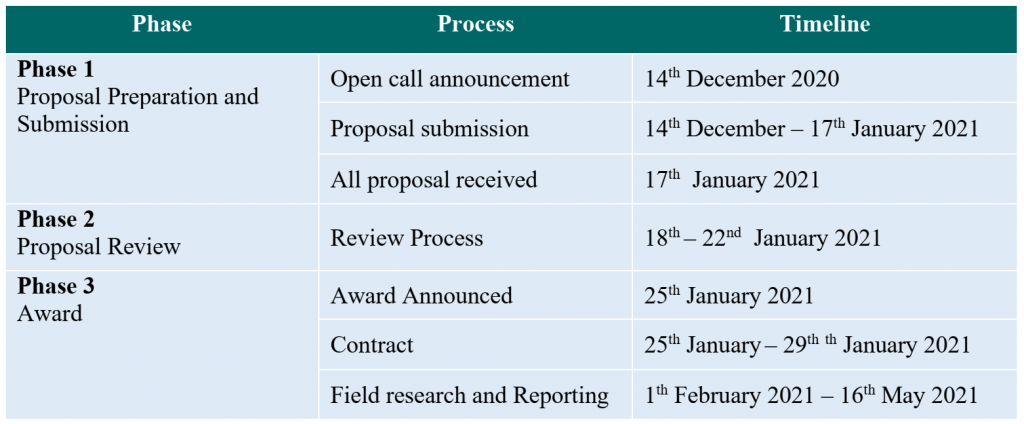

The selected applicant will be conducting one research engagement. The project is estimated to start in November 2020 and be completed by May 2021.

10.1.5. Application Process

10.2.Price Schedule Template

(See attachment)

10.3.Terms and Conditions

- The Request for Proposal is not and shall not be considered an offer by PRAKARSA.

- All responses must be received on or before the date and time indicated on the RFP.

- All proposals will be considered binding offers. Prices proposed must be valid for entire period provided by respondent.

- All awards will be subject to PRAKARSA contractual terms and conditions and contingent on the Availability of donor funding.

- PRAKARSA reserves the right to accept or reject any proposal or cancel the solicitation process at any time and shall have no liability to the proposing organizations submitting proposals for such rejection or cancellation of the request for proposals.

- PRAKARSA reserves the right to accept all or part of the proposal when award is provided.

- All information provided by PRAKARSA in this RFP is offered in good faith. Individual items are subject to Change at any time, and all bidders will be provided with notification of any changes. PRAKARSA is not Responsible or liable for any use of the information submitted by bidders or for any claims Asserted therefrom.

- PRAKARSA reserves the right to require any bidder to enter into a non-disclosure agreement.

- The bidders are solely obligated to pay for any costs, of any kind whatsoever, which may be incurred by bidder or any third parties, in connection with the Response. All responses and supporting documentation shall become the property of PRAKARSA, subject to claims of confidentiality in respect of the response and supporting documentation, which have been clearly marked confidential by the bidder.

- Any product of the RFP is belong to PRAKARSA and any publication outside PRAKARSA should be consultated with and receive permition from PRAKARSA.

{kind=link}